Bond Yields Are Up, but What Are the Risks?

After years of low yields, bonds are offering higher yields that may be appealing to investors regardless of their risk tolerance. While bonds could play a role in any portfolio, they can be a mainstay for retirees looking for stability and income, and near-retirees might consider shifting some assets into bonds in preparation for retirement.

Bonds are generally considered to have lower risk than stocks — one good reason to own them — but they are not without risk. In fact, bonds are subject to multiple risks. In considering the brief explanations below, keep in mind that coupon rate refers to the interest paid on the face value of a bond, whereas yield refers to the return to the investor based on the purchase price. A bond purchased for less than face value will have a higher yield than the coupon rate, and a bond purchased for more than face value will have a lower yield than the coupon rate.

Interest rate risk (or market risk) — the risk that interest rates will rise, making the coupon rate on an existing bond less appealing because new bonds offer higher rates. This typically lowers the value of a bond on the secondary market, but it would not change the yield for a bond purchased at issue and held to maturity. As the Federal Reserve has rapidly raised rates to combat inflation, the potential resale value of existing bonds has plummeted. However, rates may be nearing a peak, which potentially could make it a more opportune time to purchase bonds. If interest rates drop, the value of a bond will typically increase.

Duration risk — the risk that longer-term bonds will be more sensitive to changes in interest rates. Duration is stated in years and based on the bond’s maturity date as well as other factors. A 1% increase in interest rates typically will decrease a bond’s value on the secondary market by 1% for each year of duration. For example, a bond with a duration of seven years can be expected to lose 7% of its value on the secondary market.

Opportunity risk (or holding period risk) — the risk that you will not be able to take advantage of a potentially better investment. The longer the term of a bond, the greater the risk that a more attractive investment might arise or other events might negatively impact your bond investment.

Inflation risk — the risk that the yield on a bond will not keep up with the rate of inflation. This might be of special concern in the current environment, but high inflation is the reason that the Fed has been raising interest rates. If inflation cools, bonds with today’s higher yields could outpace inflation going forward.

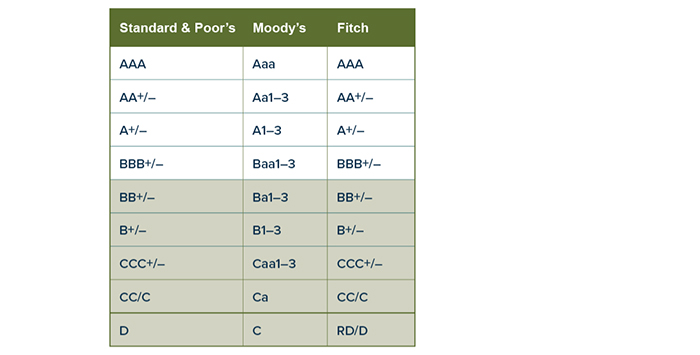

By the Letters

Bond ratings in descending order of creditworthiness as judged by the three best-known rating agencies (shaded ratings are considered non-investment grade)

Note: Standard & Poor’s and Fitch Ratings use the symbols + and – to denote the upper and lower ranges of ratings from AA to CCC; Moody’s uses the numbers 1, 2, and 3 to denote the upper, middle, and lower ranges from Aa to Caa.

Call risk — the risk that an issuer will redeem the bond when interest rates are falling in order to issue new bonds at lower rates. Investors can avoid this risk by purchasing non-callable bonds.

Credit risk (or risk of default) — the risk that the bond issuer is unable to make promised interest payments and/or return principal upon maturity. Credit-rating agencies analyze this risk and issue ratings that reflect their assessment. Higher-rated bonds are considered “investment grade.” Lower-rated bonds, commonly called “junk bonds,” are non-investment grade. They generally offer higher yields and are considered speculative with higher credit risks.

Some lower-rated bonds may be insured, so the bond carries two ratings, one for the bond and one for the insurance company. Bond insurance adds a potential layer of protection if an issuer defaults, but it is only as good as the insurer’s credit quality and ability to pay. An investor should not buy bonds based solely on the insurance.

The principal value of bonds may fluctuate with market conditions. Bonds redeemed prior to maturity may be worth more or less than their original cost. Investments seeking to achieve higher yields also involve a higher degree of risk.