Could an HSA Strengthen Your Retirement Strategy?

By one estimate, some couples who retire at age 65 in 2025 could spend as much as $428,000 on health-care expenses in retirement. This figure includes lifetime premiums for Medicare, supplemental insurance, deductibles, coinsurance, and other out-of-pocket costs for medical care and prescription drugs.1

The primary purpose of a health savings account (HSA) is for workers to set aside pre-tax income to pay current and future medical expenses not covered by health insurance. This is why HSAs are sometimes called medical IRAs. They incentivize saving with three powerful tax advantages: (1) the dollars you contribute are deducted from your adjusted gross income, (2) investment earnings compound tax-free inside the HSA, and (3) withdrawals are untaxed if the money is spent on qualified health-care expenses. (Depending on the state, HSA contributions and earnings may or may not be subject to state taxes.)

Another benefit is that account funds not needed for health expenses are available for any other purpose after you reach age 65. When HSA money is spent on anything other than qualified medical expenses, withdrawals are taxed as ordinary income, but they don’t incur the 20% penalty that applies to taxpayers under age 65.

Higher deductibles

To be eligible to establish or contribute to an HSA in 2026, you must be enrolled in a qualifying high-deductible health plan (HDHP) with a deductible of at least $1,700 for individuals, $3,400 for families.

Qualifying HDHPs also have out-of-pocket maximums, above which the insurer pays all costs. In 2026, the upper limit is $8,500 for individual coverage ($17,000 for family coverage), but plans may have lower caps. This feature could help you budget accordingly for a worst-case scenario.

Premiums are typically lower for HDHPs than they are for traditional health maintenance organization (HMO) and preferred provider organization (PPO) health plans; members usually pay more up front for services such as physician visits, surgical treatment, and prescriptions, but they typically receive the insurer’s negotiated discounts.

Contribution rules

The maximum HSA contribution limit is $4,400 if you have individual coverage or $8,750 if you have family coverage in 2026. An additional $1,000 can be contributed starting the year you turn 55. Some employers make an annual contribution to employees’ HSAs.

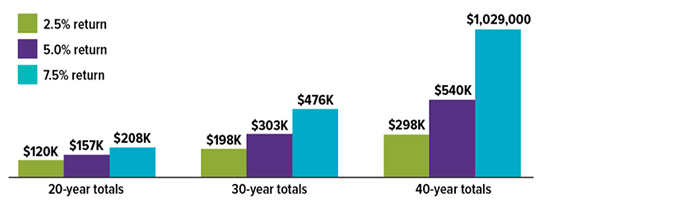

Start Young for a Chance to Amass a Million

This chart illustrates how workers might accumulate large sums by making the maximum HSA contributions annually for several decades without taking withdrawals from the account. It assumes that account owners can afford to pay their medical expenses out of pocket over their lifetime.

Hypothetical HSA balances for workers who make maximum contributions (including catch-ups), by average annual rate of return

This hypothetical example is used for illustrative purposes only and does not represent the performance of any specific investment. Actual results will vary.

Source: EBRI via Employee Benefit News, 2024

Account management

A well-funded and carefully managed HSA could play an important role in your long-term retirement strategy. Although HSA funds cannot be used to pay regular health plan premiums, they can be used for Medicare premiums and qualified long-term care insurance premiums and services during retirement. Once you sign up for Medicare, however, you can no longer contribute to an HSA.

If you can afford to fund your HSA generously while working, some of those dollars could be left untouched to compound on a tax-deferred basis for a number of years. When HSA balances reach a certain threshold, the money can be steered into a paired account with investment options similar to those typically offered in a workplace 401(k).

If you pay current medical expenses out of pocket, the accumulated HSA assets could be preserved for retirement. But save your receipts — you may want to reimburse yourself down the road if you have an unexpected cash crunch.

All investing involves risk, including the loss of principal, and there is no guarantee that any investment strategy will be successful.