The Evolution of Retirement Savings

The retirement savings landscape has changed dramatically over the past 50 years, starting with the introduction of traditional IRAs in 1975. The 1980s and ’90s brought 401(k)s, other workplace plans, and Roth IRAs; the early 2000s welcomed health savings accounts (HSAs); and over the last decade, state-sponsored retirement savings plans came into existence. Most recently, 2025 introduced 530A accounts (also known as “Trump Accounts”), which could have a positive impact on wealth-building for some of the youngest Americans. How might these and other developments affect tomorrow’s retirees?

Automatic features

In early December 2025, The Wall Street Journal reported that the number of “401(k) millionaires” reached the highest level ever, with more plan money invested in the stock market than ever before.1 One contributing factor could be the increase in automatic and default plan features over the past two decades.2 Designed to help make work-based retirement saving easy, such features include automatic plan enrollment, auto contribution increases, and diversified default investments that include stocks. Since research shows that employees who are automatically enrolled tend to remain in the plan and in the default investments,3 automatic features are likely here to stay. In fact, the SECURE 2.0 Act passed in 2022 included a provision that required most new retirement plans established after December 29, 2022, to include certain automatic features.

State-sponsored plans

However, not all workers benefit from automatic features — or retirement plans in general — since just 54% of businesses with fewer than 50 employees offered a retirement plan in 2024.4 In recent years, the federal government has tried to address this through tax benefits designed to encourage small businesses to adopt plans. Interestingly, state legislation may have an even stronger impact. Why? Unlike federal incentives, many current state laws require employers to offer a retirement savings plan.

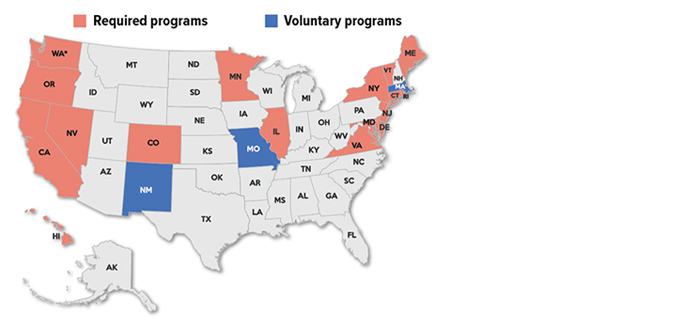

As of January 2026, 20 states have enacted state-sponsored retirement programs, growing at the rate of one to two per year since 2012. Of the 20, 17 are mandated auto-IRA programs. Every state except South Dakota has at least explored offering such plans.5

Saver’s Match

Since the first tax benefits associated with IRAs, the federal government has encouraged workers to take charge of their own futures. Currently, low-income workers receive a federal tax credit for saving in a workplace plan or IRA. However, beginning in 2027, this Saver’s Credit will be replaced by a Saver’s Match. Through this program, the federal government will match 50% of an individual’s contributions up to $2,000 (maximum $1,000 match), to be invested directly into their retirement accounts. Income limits apply.

State-Sponsored Retirement Programs

*Mandated program takes effect in 2027.

Source: Georgetown University’s Center for Retirement Initiatives, January 2026

530A accounts

Parents and guardians may open these new accounts to help children get a head start on the road to retirement. Beginning in July 2026, employers, parents, and others may make contributions to the accounts for any eligible child under 18. Moreover, for all eligible children born between January 1, 2025, and December 31, 2028, the federal government will make one-time $1,000 contributions. Total annual contributions cannot exceed $5,000 per year, per child, and accounts will be invested in low-cost index investments. Distributions will not be permitted until the child reaches age 18, at which time, the accounts generally will be subject to the same rules as a traditional IRA.

Is the future bright?

When viewed together, automatic plan features, state-mandated plans, the Saver’s Match, and 530A accounts paint a potentially bright picture for today’s younger generations; however, legislators will need to ensure that programs are designed to be easy to use and easy to understand. Awareness and education will be keys to success.